India isn't a low-trust society. It's a high-verification one

Why Kunal Shah got the evidence right but the diagnosis wrong.

I work in lending, which means I spend most of my time on a single unglamorous question. How do you part with money you may never see again, to someone you have never met?

For years I had a tidy answer, borrowed from Kunal Shah, who frames it better than most. India is a low-trust society. He points to evidence we all recognise. We check the fuel meter reads zero before the attendant starts pumping. We recount the cash the ATM just dispensed. We re-add the restaurant bill by hand before paying it. His explanation is that our sheer diversity makes trust expensive — we find it easy to trust people who share our traits, and difficult to trust people who don’t.

I accepted that framing for a long time. I’ve stopped.

What we call distrust is mostly just verification

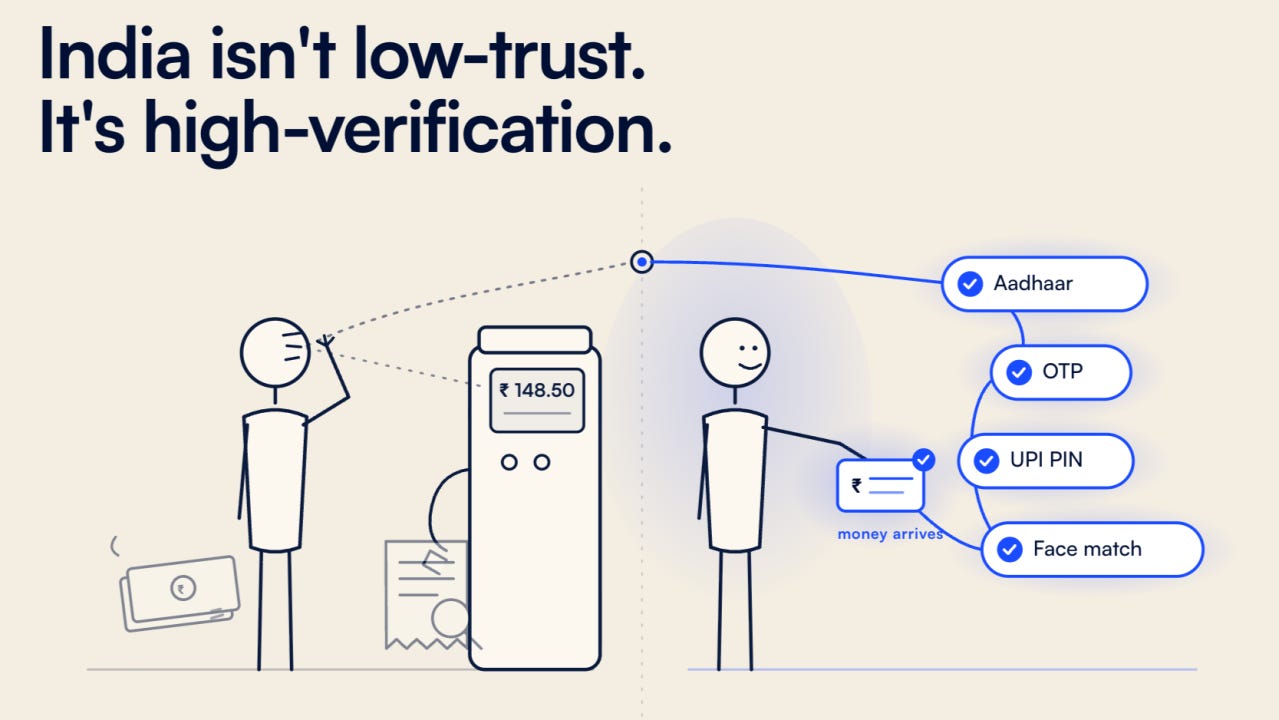

Look again at those examples. Checking the meter, recounting the cash, re-totalling the bill — none of them are quite acts of distrust. They are acts of verification. We are not refusing to transact. We are transacting, and checking as we go. The distinction sounds academic until you notice that it inverts the whole diagnosis. A low-trust society avoids the exchange. A high-verification society completes the exchange, but demands proof at every step.

And proof is the thing India has built an extraordinary, almost obsessive infrastructure for. Consider what a single small loan now asks of a borrower. Prove who you are (Aadhaar). Prove you live where you say (address checks). Prove you earn what you claim (bank statements). Prove you’re holding the phone (OTP). Prove it’s really your face (video KYC). Prove you meant to send the money (UPI PIN). We did not respond to a trust deficit by giving up on strangers. We responded by building some of the most elaborate machinery on earth for verifying them.

We ran Fukuyama backwards

Which suggests fintech has been quietly solving a different problem than the one on the label.

In Trust, Francis Fukuyama made an argument economists had circled for decades. Trust is valuable largely because it lowers transaction costs. High-trust societies can transact on a handshake; low-trust ones fall back on detailed contracts and enforcement to do the same work. The usual reading is that trust comes first, and cheap transactions follow.

The machinery we built runs that causation backwards. We did not become more trusting and then transact more freely. We made verification so cheap that the question of trust mostly stopped needing to be asked.

That is what every product I admire actually does. UPI doesn’t persuade you to trust the recipient’s bank; the money simply arrives, and the rails settle it out of sight. Stripe doesn’t convince a developer it’s reliable; payments work, and the proof is the absence of incident. Amazon doesn’t ask a buyer to trust a seller they’ve never heard of; the returns policy closes the loop, so the buyer never has to. In each case the product didn’t manufacture trust. It removed the moment where trust had to be negotiated at all.

Yes, this looks a lot like surveillance

The fair objection is that this isn’t trust, it’s surveillance wearing trust’s clothes. If I only “trust” you because Aadhaar, a bureau, and a face-match algorithm have vouched for you, the warmth has gone out of the word.

It’s a fair point, and I don’t want to wave it away. But notice what it concedes. The behaviour that looks like trust, handing money to a stranger or shipping goods before the payment clears, happens anyway. The lived experience of a high-trust society is people transacting freely with strangers. We are increasingly getting that experience. We’re just getting it through infrastructure rather than disposition.

The lever was never trust

Which raises a more useful question for anyone building here. If trust is downstream of verification cost, then the lever was never “earn trust”, a vague, slow, brand-led project. The lever is making the next proof cheaper than the last. Every point you shave off the cost of verifying someone widens the circle of people you can safely transact with. That is the real story of India’s last decade. Each time we drove the cost of one proof toward zero — identity with Aadhaar, payment with UPI, consent with the Account Aggregator framework — a fresh layer of strangers became reachable.

There’s a catch, and I’d rather not gloss over it. Cheap verification is not free verification, and the costs don’t vanish, they move. They land on the people least able to produce clean proof: the borrower with a thin file, the migrant whose address never matches the database, the worker whose income arrives in cash. For them, a high-verification society can exclude more sharply than a low-trust one, because the door is open but the keys are documents they don’t have. The frontier of this work isn’t more verification. It’s verification that works for people whose lives don’t generate tidy records.

A society that stops noticing

So I’d offer a small amendment to Kunal’s framing, less a correction than a sequel. India isn’t low-trust. It’s pre-verification, a place where trust was historically expensive because checking strangers was expensive, and where the whole fintech project has been an effort to drive that checking cost down.

Maybe that’s how societies actually become higher-trust over time. Not because people grow more virtuous, but because the cost of proof keeps falling — until one day we look up and realise we’ve been trusting strangers all along, and simply stopped noticing the machinery that let us.